18 Jan We Didn’t Light It, We Tried To Fight It 01.11.24

Chief Investment Officer

As I reflect on 2023, I’m reminded of Billy Joel’s famous song, “We Didn’t Start the Fire”, in which he lists major historical events over a 40-year time frame. Many of the moments in time reference conflict and economic stress. This past year, we had plenty of fires with bank failures, continued fighting in Ukraine, decade-high mortgage rates, conflict in Gaza, and persistent inflation. We certainly did not start the inflation fire, rather those seeds had been sown by decades of loosening monetary policy, culminating with a pandemic-induced deluge of stimulus placed directly into consumers’ pockets.

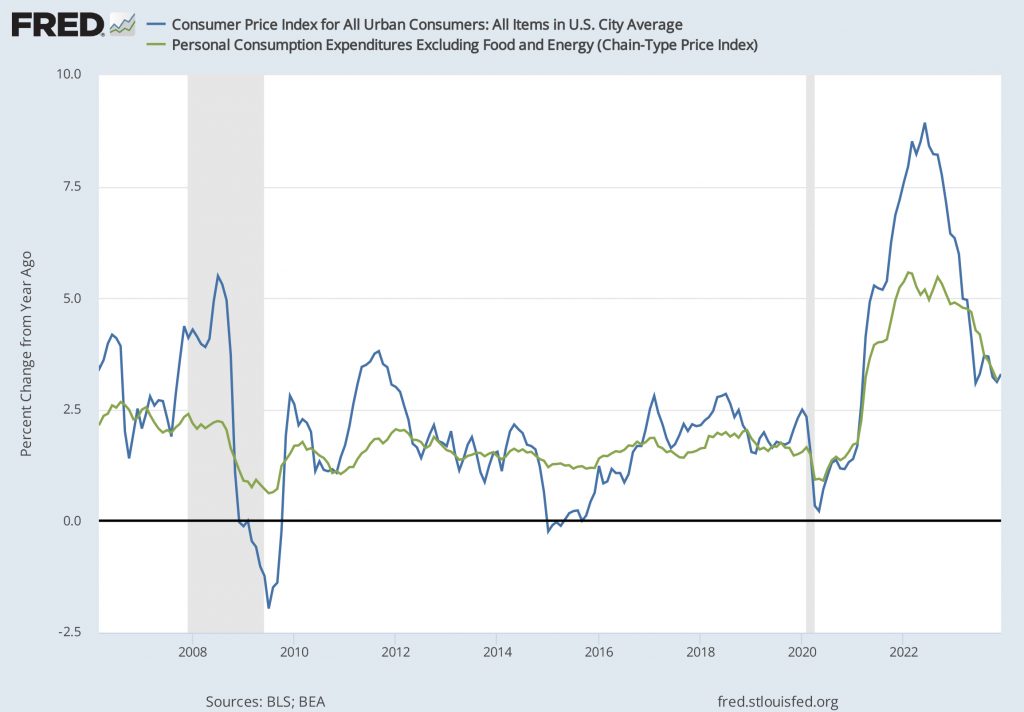

As in 2008, and more recently in 2020, there were plenty of reasons to abandon the markets in 2023. In fact, most economists predicted (with absolute certainty) a recession was in the cards. Between all the fires and negative predictions, many investors headed for safety and were somewhat rewarded until the last quarter of the year, when those who abandoned the markets missed out on significant returns. Cooling core CPI (a broad inflation gauge – shown below) was the trigger, and it combined with oversold equity and bond markets for one of the largest quarterly rallies for balanced portfolios in history.